Mastering profit and loss: A Practical Guide to Freelance Finances

Let's think of your freelance business as a road trip. Your Profit and Loss (P&L) statement is your trusty map. It shows you exactly where you've been financially over a certain period—a month, a quarter, or a year. Most importantly, it answers the one question every business owner loses sleep over: am I actually making money?

Think of it as your business's report card.

What Is a Profit and Loss Statement?

A P&L statement, sometimes called an income statement, is a straightforward summary of all your income and all your outgoings over a set period. It’s not just a box-ticking exercise for your accountant; it’s a powerful tool that helps you see your business clearly and make smart decisions.

At its core, a P&L tells a simple story. It starts with everything you've earned (your revenue), then subtracts everything you've spent to run your business (your costs and expenses).

What’s left at the end is your net profit or net loss—the famous "bottom line." It's the truest measure of how your business is actually performing.

Why It Matters for Freelancers

As a freelancer or consultant, getting a handle on your P&L is what separates a hobby from a real business. It moves you from just chasing invoices to strategically building something that lasts. A clear P&L gives you the kind of insights that let you take control.

When you apply for a loan or credit, lenders will almost always ask for a P&L statement. It gives them a snapshot of your financial health—how much you're bringing in, how you manage costs, and whether you're profitable. It's how they figure out if you're a good risk.

By checking in with your P&L regularly, you can:

- Price Your Services With Confidence: Are your rates actually covering your costs and leaving you with a decent profit? Your P&L will tell you.

- Spot Money Drains: Notice that software subscription you forgot about? Or that your marketing costs are creeping up? A P&L makes it easy to spot where your money is going and cut back where needed.

- Plan for the Future: Use your past performance to make realistic financial forecasts. It helps you decide when it's the right time to invest in new equipment, take a course, or launch that new marketing campaign.

A Simple Analogy: The Freelance Writer

Let's make this real. Imagine a freelance writer has a good quarter and brings in €5,000 from various client projects. That's their total revenue.

Now, let's tally up the costs of running their business during that same period:

- Software Subscriptions: €150 (for writing tools and project management apps)

- Marketing: €200 (for a professional portfolio website and a few social media ads)

- Home Office Costs: €300 (a reasonable portion of rent, utilities, and internet)

- Professional Development: €250 (for an online course to sharpen their skills)

Their total expenses add up to €900. The final step is simple maths:

Revenue (€5,000) - Expenses (€900) = Net Profit (€4,100)

That €4,100 is what the writer actually earned. It’s the real profit left over after paying for everything needed to run the business. This simple calculation cuts through the noise and gives them a clear, tangible measure of their success, which is exactly the kind of clarity you need to steer your business in the right direction.

What Are the Key Parts of a P&L Statement?

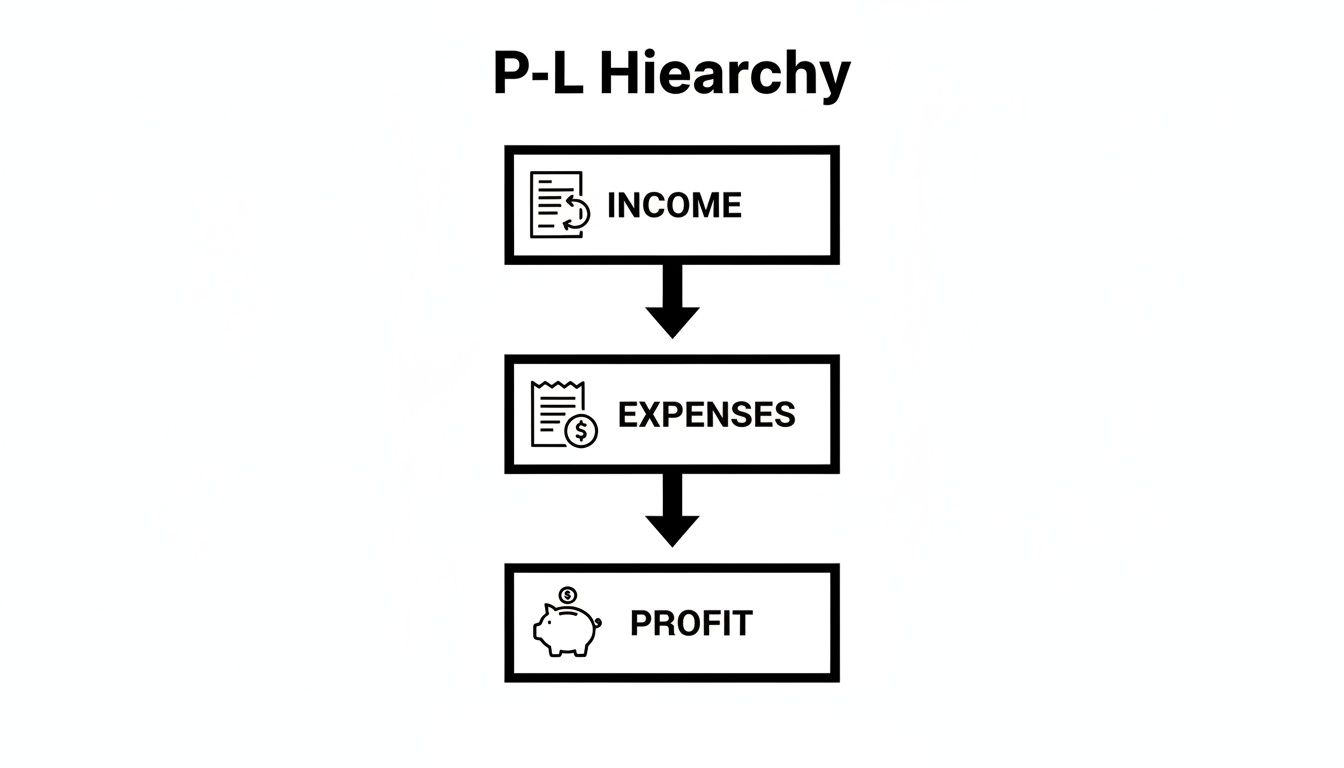

Think of your P&L as the story of your business's financial health over a specific period. To really get it, you need to know the main characters in that story. It’s a simple, logical journey that starts with everything you’ve earned and ends with what you actually get to keep.

Revenue: The Starting Point

Right at the top of the P&L, you’ll find Revenue. This is your headline number—the total amount of money you've brought in from selling your services or products. Everything else flows from here.

For a freelance web developer, revenue is simply the sum of all client invoices. If you billed three projects in a quarter for €5,000, €3,000, and €7,500, your total revenue for that period is €15,500. This is your gross income before a single cost has been touched.

This simple diagram shows the basic formula at work.

As you can see, profit isn’t just about the money coming in; it’s about what’s left after you've paid for everything it took to earn that money.

Cost of Goods Sold and Gross Profit

Next, we subtract the Cost of Goods Sold (COGS). Now, that term might sound like it’s only for businesses selling physical items, but it’s just as important for freelancers. COGS are any direct costs linked to delivering your service.

So, what counts as COGS for a freelancer?

- Subcontractor Fees: The money you paid another freelancer to help you out on a specific client project.

- Project-Specific Software: A special plugin or software licence you had to buy exclusively for one client’s job.

- Direct Materials: For a graphic designer, this could be the cost of getting a client's brochures professionally printed.

Subtracting COGS from your Revenue gives you your Gross Profit. This figure is gold. It tells you exactly how profitable your core services are before you factor in your general business overheads.

Operating Expenses

Once you have your gross profit, it's time to look at your Operating Expenses (OpEx). These are the costs of keeping the lights on—the day-to-day expenses you have to pay just to run your business, whether you have client work or not.

Common operating expenses for freelancers include things like:

- Marketing and advertising spend

- Monthly software subscriptions (like your project management tool)

- Internet and phone bills

- Professional insurance

- Home office expenses

These are the overheads that keep your operation afloat. Adding them all up shows you what it costs to simply open for business each month.

Your P&L isn't just a stuffy document for tax time. It’s a crucial health check. Lenders often ask for one to see if your income is stable and if you can handle a loan, making it a foundation of your business’s credibility.

Net Profit: The Bottom Line

Finally, we get to the most anticipated number on the P&L: Net Profit. This is the famous "bottom line," and it shows you what your business really made.

The calculation couldn't be simpler:

Gross Profit - Operating Expenses = Net Profit

If you end up with a positive number, fantastic—your business is profitable! If it’s negative, you’ve got a net loss for that period. This single figure, more than any other, tells you how much money your business has genuinely generated after every single bill has been paid. It's the ultimate report card for your financial performance.

P&L vs. Other Key Financial Reports

Looking at a profit and loss statement on its own is like trying to understand a football match by only looking at the final score. You see who won, but you miss the whole story. To get a complete picture of your business's financial health, you need to look at the P&L alongside two other key reports: the Balance Sheet and the Cash Flow Statement.

Think of them as three different camera angles on your business finances.

- The Profit and Loss Statement is the action-packed highlight reel. It shows your performance over a period—a month, a quarter, a year—tallying up your income and expenses to reveal if you came out ahead.

- The Balance Sheet is a sharp, still photograph. It captures your business's financial position at a single, specific moment in time. It's a snapshot of everything you own (assets) and everything you owe (liabilities).

- The Cash Flow Statement is like a candid, behind-the-scenes video. It tracks the real-time movement of money into and out of your bank account, showing where your cash actually comes from and where it goes.

The P&L and the Balance Sheet

The biggest difference between these two is time. A P&L tells a story over a period, answering the question, "How did my business do last quarter?" It’s all about performance and profitability.

A Balance Sheet, on the other hand, is a statement of fact at one specific point in time, like close of business on 31 December. It focuses on your overall financial structure, answering, "What is my business worth right now?"

Profit vs. Cash: The Most Critical Distinction

This is the one that trips up so many freelancers and small business owners. It’s entirely possible for your P&L to show a fantastic profit while your bank account is frighteningly empty. This gap between profit on paper and cash in hand is a very common—and dangerous—trap.

So, how does that happen? Your P&L usually works on an accrual basis, meaning you record income when you earn it (i.e., when you send an invoice), not necessarily when the client pays you. That €10,000 invoice you sent last month makes your profit look great, but until that money actually lands in your account, it’s just a number on a spreadsheet.

The Cash Flow Statement is your dose of reality. It ignores the promises and only tracks the actual pounds and pence moving in and out of your business. It tells you if you have enough cold, hard cash to pay your rent and suppliers tomorrow.

To bring this home, consider the current economic climate. Recent reports on Luxembourg's financial sector performance show that even major banks are seeing their profitability squeezed. This can have a ripple effect, sometimes leading to slower payment cycles from your clients. Understanding your cash flow helps you build a buffer and anticipate these delays before they become a crisis.

To make these distinctions even clearer, let's break them down in a table.

P&L vs Balance Sheet vs Cash Flow Statement

| Financial Statement | What It Shows | Timeframe | Key Question Answered |

|---|---|---|---|

| Profit & Loss (P&L) | Your company's financial performance and profitability. | Over a Period (e.g., month, quarter, year) | "Did we make or lose money?" |

| Balance Sheet | Your company's financial position and net worth. | A Single Point in Time (e.g., as of Dec 31st) | "What do we own and what do we owe?" |

| Cash Flow Statement | The movement of actual cash in and out of your business. | Over a Period (e.g., month, quarter, year) | "Where did our cash come from and where did it go?" |

Ultimately, you need all three to steer your business effectively. The P&L shows if your business model is working, the Balance Sheet gives you a measure of your stability, and the Cash Flow Statement confirms you have the actual money to keep the lights on. Together, they give you the complete, 360-degree view you need to make smart decisions.

How to Create Your First Profit and Loss Statement

Ready to stop guessing about your business's financial health? Creating your first profit and loss statement isn't about getting bogged down in complex accounting; it's really just organised addition and subtraction. Think of it as turning a pile of numbers into a clear story about how you've performed.

This guide will walk you through the process step-by-step, removing any guesswork. We’ll start with gathering your records and finish by calculating that all-important bottom line.

Step 1: Gather All Your Financial Records

Before you can crunch a single number, you need to pull together your raw materials. This means collecting every piece of paper (digital or physical) related to the money that came in and went out of your business during a specific period, like last month or the last quarter.

Here’s what you’ll need to round up:

- All Client Invoices: Every single invoice you sent out during the period. This is the foundation of your revenue.

- Business Expense Receipts: Grab receipts for everything you bought for your business, from software subscriptions to a new keyboard.

- Bank and Credit Card Statements: These are perfect for double-checking your records and catching any small expenses you might have forgotten.

A solid system for your paperwork makes this step a breeze. If you feel like you’re drowning in documents, check out our guide on how to track freelance invoices for some practical tips.

Step 2: Calculate Your Total Revenue

With your records in hand, it’s time for some simple maths. Start at the top: add up the total value of all the invoices you issued during your chosen period. This gives you your total revenue, also known as gross income.

For instance, if you invoiced three clients for €2,000, €3,500, and €1,500 in a quarter, your total revenue for that period is €7,000. This is your starting point.

Step 3: Determine Your Direct Costs

Next up are the direct costs you incurred to deliver your services. For freelancers and consultants, this is often called the Cost of Goods Sold (COGS), even if you’re not selling physical goods. These are the expenses that are directly tied to a specific client project.

Here's a simple way to think about it: if you didn't have the project, you wouldn't have had the cost. That's a direct cost. It could be hiring a subcontractor for a tricky part of a job or buying a specific software licence that was only needed for one client's work.

Add up these project-specific costs. Let's say you paid a subcontractor €500 for work related to that €7,000 in revenue. Your COGS is €500.

Now, subtract this from your revenue (€7,000 - €500) to find your Gross Profit, which comes out to €6,500.

Step 4: Tally Your Operating Expenses

Now it's time to account for the everyday costs of simply running your business. These are your operating expenses—the bills you have to pay to keep the lights on, whether you have a dozen clients or none at all.

This category includes things like marketing costs, professional insurance, your internet bill, and ongoing software subscriptions. Add them all up. For our example, let's say your total operating expenses for the quarter were €1,200.

Step 5: Calculate Your Net Profit

This is the final step, where it all comes together. To find your net profit, you just subtract your total operating expenses from your gross profit. It's that simple.

Gross Profit (€6,500) - Operating Expenses (€1,200) = Net Profit (€5,300)

That €5,300 is your "bottom line"—the actual profit your business made. Getting this number right is more important than ever, especially with shifting tax laws. For example, recent corporate income tax reductions in Luxembourg mean freelancers can potentially keep more of what they earn. An accurate P&L is essential to make sure you're taking full advantage of these fiscal changes, as highlighted in insights about the Luxembourg fiscal outlook 2025.

Using Your P&L to Make Smarter Business Decisions

A profit and loss statement is so much more than a document you dust off for tax season. Think of it as a roadmap for your business's future. Once you get comfortable with what it’s telling you, you can use it to analyse what’s working, spot hidden opportunities, and make sharp, data-driven decisions that actually lead to growth. This is the point where your P&L stops being a simple report and becomes your most powerful strategic tool.

When you look past the raw numbers, you start to see the story they tell. Is one of your services a quiet superstar, consistently bringing in high profits? Are certain expenses creeping up, month after month, eating into your bottom line? Your P&L has all the answers, helping you steer your freelance business with confidence instead of just guessing.

Analysing Key Profitability Metrics

To really unlock the insights hiding in your P&L, you need to look at a couple of key calculations. One of the most important is the Net Profit Margin. This simple metric tells you exactly how much profit you’re making for every euro of revenue you bring in.

The formula is straightforward:

(Net Profit / Total Revenue) x 100 = Net Profit Margin

Let's say you had a net profit of €5,000 on total revenues of €20,000. Your net profit margin would be 25%. That means for every single euro you earned, you got to keep 25 cents as pure profit. Tracking this figure over time is the best way to see how financially healthy and efficient your business truly is.

Another vital number to watch is your cost-to-income ratio. It measures your operating expenses against your revenue, showing how much it costs you to make a euro. A rising ratio is an early warning sign that your costs are starting to grow faster than your income. This isn't just a concern for freelancers; it’s a key health indicator for entire industries. For example, recent figures from Luxembourg’s banking sector showed the cost-to-income ratio climbing, a signal that operational expenses were outpacing revenues for many big institutions. You can see more on Luxembourg's banking sector performance. For a freelancer, this wider trend is a great reminder to keep a close eye on your own ratio.

Spotting Trends and Making Adjustments

Getting into the habit of reviewing your P&L—whether it’s every month or every quarter—is how you spot trends before they become serious problems. Are your software subscriptions starting to balloon? Did that recent marketing campaign actually deliver a decent return on investment?

Look for patterns in both your income and your expenses:

- Income Trends: Pinpoint which of your services are the most profitable. This kind of insight helps you focus your marketing efforts or even decide to specialise in a high-margin area.

- Expense Trends: Identify costs that are slowly but surely increasing. This could be anything from professional fees to office supplies. Catching these early gives you the chance to find more cost-effective alternatives before they get out of hand.

By comparing your P&L statements from one period to the next, you turn raw data into actionable intelligence. This consistent analysis is what enables strategic decisions, like knowing precisely when it’s the right time to raise your rates or invest in new equipment.

For instance, if your P&L shows that your profit margin is shrinking even though your revenues are going up, it’s a clear signal that your expenses are running wild. That data gives you the confidence to make the necessary changes, whether it’s cutting a non-essential subscription or renegotiating terms with a supplier. These moves are crucial for protecting your bottom line. A solid P&L is also the foundation for figuring out how to price your freelance projects for maximum profitability.

Common P&L Mistakes to Avoid

Getting your finances right is a journey, not a destination. But a few common slip-ups on your profit and loss statement can paint a completely false picture of how your business is actually doing. Dodging these classic pitfalls is the key to turning your P&L into a reliable map for growth, not just another confusing spreadsheet.

Think of your P&L as the annual health check-up for your freelance business. An accurate report helps you make smart decisions, while a flawed one can send you chasing phantom profits or panicking over non-existent problems. When you get this right, the story your numbers tell is the true one.

Mixing Business and Personal Expenses

This one is the cardinal sin of freelance finance, and it's shockingly easy to commit. You use the business card for a personal dinner out, or you buy a new work laptop with your personal money and forget to log it properly. Just like that, your financial data is compromised.

The result? Your P&L ends up with bloated expenses or underestimated costs, rendering your net profit figure practically meaningless. The only way to get a true read on your business’s profitability is to draw a hard line between your business and personal finances.

A clean, accurate profit and loss statement is crucial for more than just your own planning. If you ever apply for a business loan or a mortgage, lenders will pore over your P&L to gauge your income stability. Mixing personal and business expenses throws up immediate red flags and can seriously hurt your chances of getting approved.

Inaccurate Revenue Reporting

Another frequent stumble is booking your revenue incorrectly. This usually happens when freelancers get cash flow and profit mixed up. For example, you might only record income when the money actually lands in your bank account, instead of when you've earned it and sent the invoice (which is the accrual method).

While both methods have their place, the real killer is inconsistency. It can create a spiky, misleading view of your performance, especially if you have large projects with invoices paid weeks or even months after you’ve done the work. A reliable P&L demands you pick a method and stick to it. For a deeper dive, check out our guide on essential cash flow tips for freelancers.

Forgetting to Categorise Expenses Properly

Just dumping all your outgoings into one big bucket labelled "expenses" is a huge missed opportunity. Without sorting your costs into clear categories, you have no idea where your hard-earned money is actually going.

Are you spending a fortune on software subscriptions you barely use? Is that new marketing campaign actually bringing in clients? Properly categorising your expenses helps you answer these vital questions.

- Software & Subscriptions: Keep tabs on all those recurring tool costs.

- Marketing & Advertising: See what you're spending to find new work.

- Professional Development: Track what you invest in courses and training.

- Office Supplies: Monitor the small stuff needed for day-to-day operations.

This level of detail is what transforms your P&L from a boring summary into a powerful diagnostic tool.

Neglecting Small or Non-Cash Expenses

It's so easy to let the little things slide, but remember that tiny leaks can sink a big ship. That €10 monthly subscription or the odd trip to buy printer paper might seem trivial, but these costs stack up over a year. Failing to track them means you're understating your real expenses.

Likewise, non-cash expenses like depreciation—the slow decline in value of an asset like your work computer—are often completely ignored by freelancers. While depreciation doesn't take cash out of your pocket today, it is a genuine business expense. Including it on your P&L gives you the most complete and honest financial picture possible.

Your P&L Questions, Answered

Even with a step-by-step guide, it's natural to have a few lingering questions when you're getting to grips with your P&L statement. This is where we tackle the common "what ifs" and "how oftens" that pop up for freelancers and consultants.

Think of this section as a quick chat with a trusted advisor. We'll clear up the practical details, from timing your reports to understanding what your profit margin is really telling you.

How Often Should I Run a P&L Statement?

There's no single magic number here, but a solid baseline for most freelancers is to prepare a P&L statement at least quarterly. This gives you a regular, big-picture look at how your business is performing, letting you catch trends and make course corrections without getting lost in the daily weeds.

For a more detailed view, you could try:

- Monthly P&Ls: These are perfect if your income varies month-to-month or if you're actively trying to rein in your spending. It gives you a much tighter grip on your finances.

- Annual P&Ls: This is non-negotiable. You'll need it for your tax returns and for taking a proper, end-of-year look at your business's overall performance.

The real key is consistency. Pick a rhythm that feels right for you and stick to it. Over time, you’ll build an invaluable history of your financial journey.

What’s a Good Profit Margin for a Freelancer?

This is the million-euro question, and the answer is: it depends. A freelance copywriter with minimal overheads might see a much higher margin than a video producer who has to rent expensive gear for every project.

That said, a healthy net profit margin for many service-based freelancers often lands somewhere in the 15% to 25% range. If you find yours is consistently dipping below 10%, that’s a red flag. It could mean your pricing is too low or your expenses are creeping up. On the flip side, anything above 30% is fantastic and suggests you're running a very tight ship.

Your profit margin is arguably the most vital sign of your business's health. It answers one simple question: "For every euro that comes in, how much do I actually keep?" Keeping an eye on it is the key to pricing yourself smartly and managing your costs.

Is It Possible to Show a Profit but Have No Money in the Bank?

Yes, absolutely. This is a classic trap and one of the most important lessons for any solo business owner to learn. Your P&L statement can look rosy while your bank account is empty.

Here’s how it happens: Your P&L records revenue the moment you earn it (i.e., when you send the invoice), not when the client actually pays you.

It creates a deceptively dangerous situation:

- You finish a €5,000 project and issue the invoice. On paper, your P&L just got a massive profit boost.

- But the client is on 60-day payment terms. The actual cash won't land in your account for two months.

- Meanwhile, you still have bills to pay now—software subscriptions, rent, and your own salary.

This gap between paper profit and actual cash is precisely why you can never rely on the P&L alone. You have to watch your cash flow just as closely. A profitable business can go under simply because it ran out of cash to pay its immediate bills.

What's the Difference Between Gross and Net Profit?

Getting your head around gross vs. net profit is crucial for really understanding your P&L. They each tell a different, important part of your financial story.

- Gross Profit is what's left after you subtract the direct costs of your work (your Cost of Goods Sold) from your revenue. It tells you how profitable your core services are, before accounting for all your general business overheads.

- Net Profit is your "bottom line." It’s the final amount left after you've subtracted all your expenses—both direct costs and operating expenses—from your revenue. This is what your business truly earned.

A simple way to think about it is that gross profit shows how efficient your service delivery is, while net profit reveals the overall financial health of your entire business.

Ready to stop chasing invoices and get a clear view of your business finances? Billzy organises all your invoices in one simple dashboard, projects your cash flow, and provides smart reminders to help you get paid faster. Take control of your income pipeline and see what you're really earning. Start for free and track your first 10 invoices.

Ready to Get Paid Faster?

Create professional invoices and track payments in seconds with Billzy.

Start Free Today